Compound Interest Explained With Small Numbers

A simple visual explanation of compound interest, why time matters, and what compounding can and cannot do.

Here is the tiny version:

Compounding means growth can start earning growth.

That is the whole idea. The original amount earns something. Then that amount plus the earlier growth can earn more. The second layer is where compounding starts to look interesting.

It is not magic. It is math with patience.

A Small Example

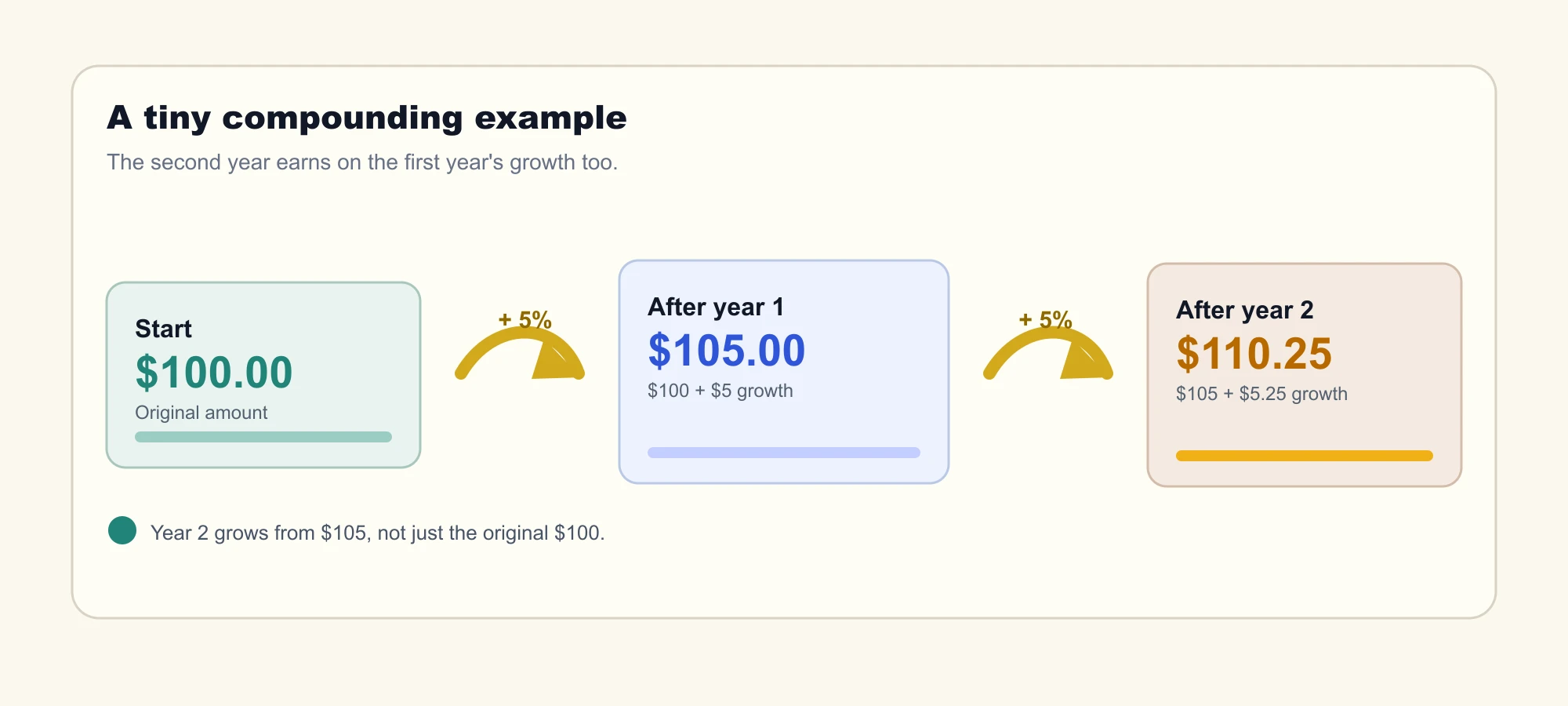

Imagine you put $100 somewhere that earns 5% in a year.

After one year, you would have $105.

If the next year also earns 5%, the 5% is not only on the original $100. It is on $105.

That means the second year’s growth would be $5.25, not $5.

The extra 25 cents is not going to retire anyone. Please do not inform your boss yet.

But the pattern matters. Over long periods, growth on top of growth can become a bigger part of the story.

Why Time Matters

Compounding likes time because time gives the layers room to build.

A single year is usually not dramatic. Five years may still feel modest. But over decades, the difference between only saving and saving plus investment growth can become meaningful.

Benjamin Franklin understood the long game in a very literal way. The Franklin Institute notes that Franklin, the printer, inventor, and statesman, set aside 2,000 pounds sterling in his will for Boston and Philadelphia and asked that the bequest be handled over a 200-year period. That is an extreme example, and most of us are not casually writing two-century plans between errands. But it shows the basic idea: time changes what growth can do.

That is one reason people talk about starting early. Starting early does not guarantee a specific result, and investments can go down as well as up. But more time gives compounding more chances to work.

The habit matters, too. A one-time deposit can compound, but regular contributions give the account more fuel.

That is why small repeatable habits, like saving $5 a day, can become more powerful after the financial foundation is ready for investing.

Saving And Investing Are Not The Same

Compounding can happen in different places, but the risk is not the same everywhere.

A savings account can pay interest. The growth is usually steadier, and the cash is easier to access. That makes savings useful for emergency funds, bill buffers, and short-term goals.

Investments can grow more over long periods, but they can also lose value. Stocks, index funds, and ETFs move around. That is normal, but it means invested funds should usually be funds you do not need for near-term emergencies.

Emergency savings should stay accessible and low-risk. Compounding is nice. Being able to pay the urgent bill is nicer when the bill is due now.

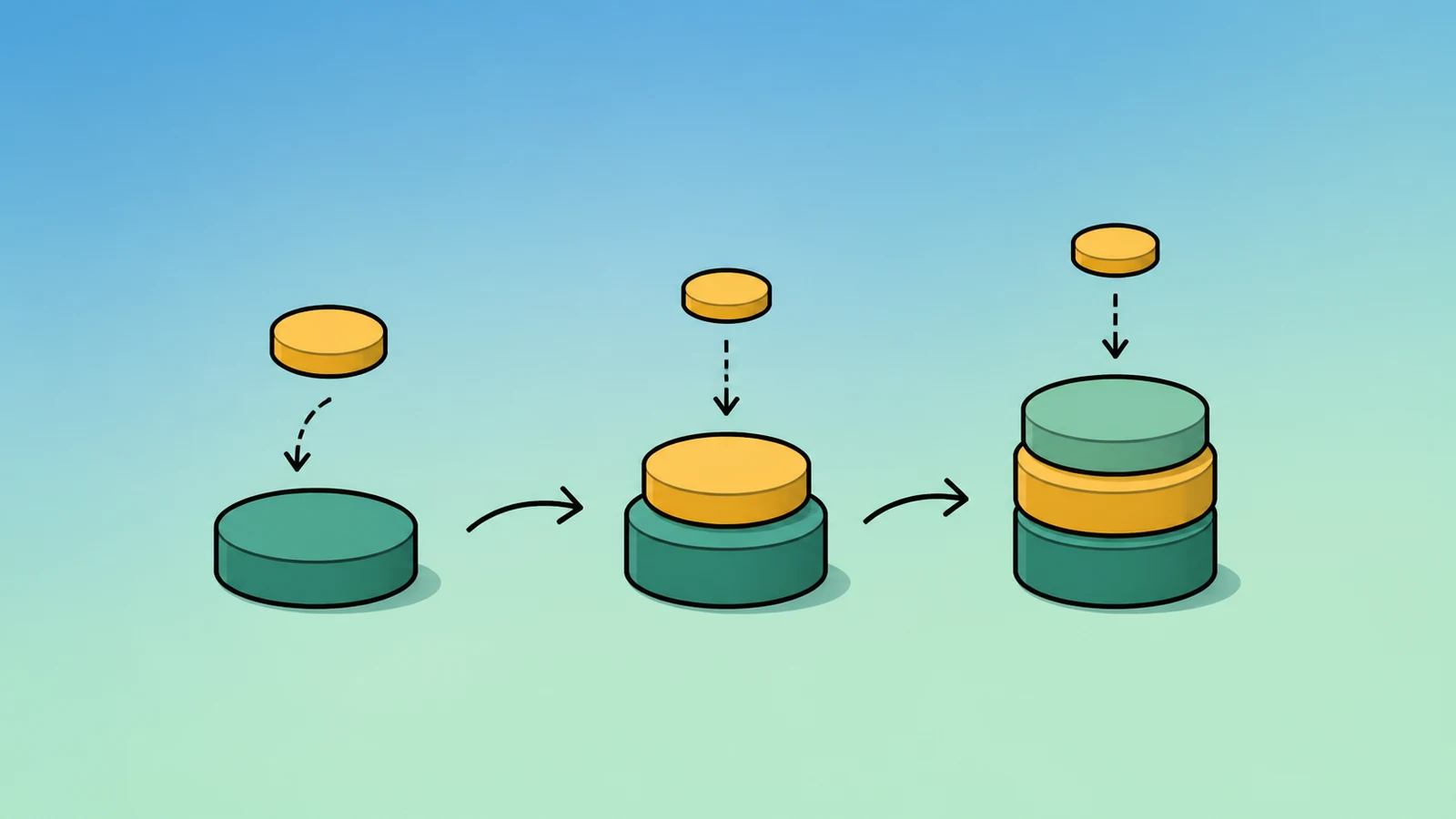

The Visual To Remember

Picture compounding like three layers:

- Money you put in.

- Growth on the amount you put in.

- Growth on the earlier growth.

The third layer is the special part.

At first, it is tiny. Later, it can become easier to see. That is why compounding rewards consistency and time more than drama.

What Compounding Cannot Do

Compounding is useful, but it is not a shortcut around reality.

It cannot fix a budget that is short every month. It cannot guarantee investment returns. It cannot make high-interest credit card debt harmless. It cannot turn a risky investment into a safe one because the chart looks exciting.

The order still matters.

Cover bills first. Build at least a small savings cushion. Be careful with high-interest debt. Then learn how long-term investing might fit.

Compounding works best when it is part of a stable plan, not a rescue mission.

Try This

Write down one number you could repeat every month.

It might be $10, $25, or $50. If your emergency savings is still thin, point that contribution there first. If your foundation is steadier, use the number to learn how regular investing contributions could work.

The lesson is simple: the earlier layers may look small, but small layers can still matter when they keep showing up.

Source note: Historical note on Benjamin Franklin’s 200-year bequest checked against The Franklin Institute’s donor story.