How To Use A Windfall Without Losing It

A practical way to handle a bonus, refund, gift, or extra paycheck before the money disappears into everyday spending.

A windfall is money that arrives outside your normal paycheck rhythm.

It might be a tax refund, bonus, gift, rebate, side-gig payout, settlement, or extra paycheck month. The amount can be large or small. The common feature is that it feels separate from regular income, which makes it weirdly easy to spend twice in your head.

The fix is to give it jobs before the money blends in.

Pause Before Spending

The first move is not a spreadsheet. It is a pause.

Give yourself a day or two before making big decisions, especially if the money is larger than usual. Fast money decisions tend to follow the loudest feeling in the room: relief, excitement, guilt, or the sudden belief that every appliance should be replaced immediately.

You do not need to freeze. Just slow the first move enough to choose on purpose.

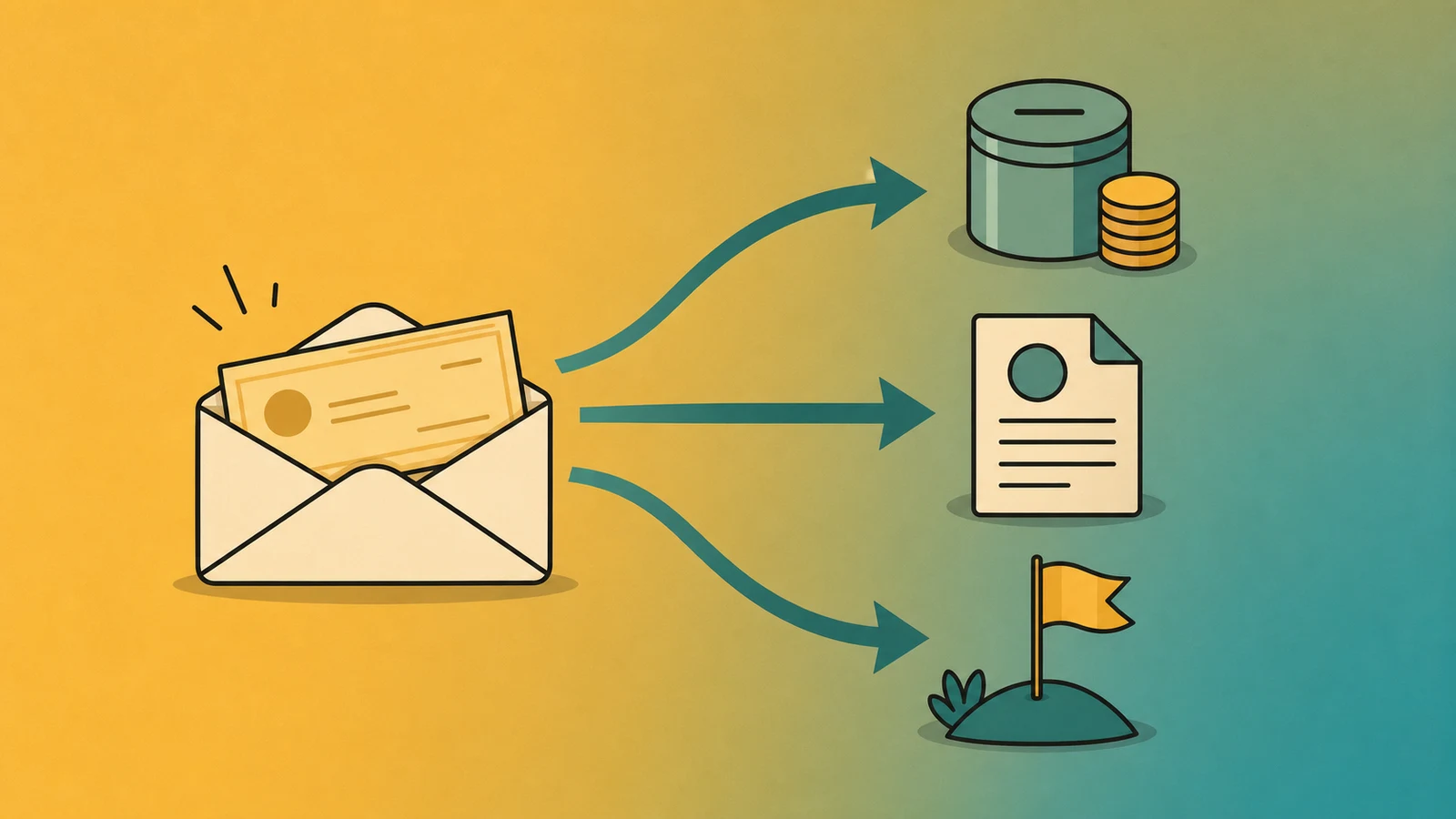

Split It Into Three Jobs

A simple windfall split can keep the decision balanced.

Consider three categories:

- Stabilize: bills, emergency savings, overdue expenses, or a checking buffer.

- Reduce pressure: high-interest debt, upcoming irregular expenses, or repairs.

- Enjoy: something useful, fun, or meaningful now.

The percentages can change. If you are behind on bills, stabilize may get most of it. If your foundation is steady, more can go toward a goal or long-term investing.

The point is to make the money serve more than one part of life.

Fix One Annoying Problem

Windfalls are useful for small problems that keep draining attention.

Maybe you need a tire replacement, dental appointment, work shoes, a bill buffer, or a savings cushion. These are not glamorous uses, but they can make the next few months easier.

If a $400 windfall prevents a $400 credit card balance later, that is a real win.

This connects closely to building a bill buffer. Sometimes the best use of extra cash is making normal bills less dramatic.

Be Careful With Permanent Upgrades

One-time money should be used carefully for ongoing costs.

A bonus can cover the first month of a nicer car payment, apartment, subscription bundle, or financed purchase. It cannot cover the next 47 months unless regular income can handle them too.

Before using a windfall to start a new recurring payment, ask whether the monthly cost still works after the windfall is gone.

If the answer is no, the windfall may be opening a door your paycheck has to keep holding.

Keep Some Joy In The Plan

Using every extra dollar for responsible purposes can sound mature, but it may not be realistic.

If the windfall is not needed for an urgent bill, consider assigning a small amount to something enjoyable. A dinner out, a short trip, a hobby item, or a useful upgrade can make the plan feel less like punishment.

This is not permission to ignore debt or savings. It is permission to build a plan a human might actually follow.

Move The Money Quickly

Once you choose the split, move the money.

Send savings to savings. Pay the debt. Put the bill buffer in checking and label the new floor. If the money sits in one big checking balance, it becomes very easy for the plan to fade.

Money without a job tends to volunteer for snacks, shipping, and mysterious household items.

Try This

Use a simple three-line windfall plan:

- First, cover anything late or urgent.

- Second, send a chosen amount to savings or debt.

- Third, keep a small planned amount for now.

A windfall does not have to change your whole life to matter. It just has to make the next step easier instead of disappearing without a trace.