How To Enjoy A Raise Without Spending The Whole Raise

A practical way to use a raise for savings, debt, and real-life enjoyment before lifestyle creep quietly absorbs it.

A raise is good news.

It is also surprisingly easy for a raise to vanish.

Not in one dramatic purchase. More like a few upgrades, some extra convenience, a subscription or two, better takeout, and suddenly the new income is just the old stress wearing nicer shoes.

That is lifestyle creep.

Enjoying a raise is not the problem. The problem is letting the raise disappear before it has a job.

The First Move Is A Pause

Before changing your spending, pause for one paycheck.

Let the new paycheck arrive. Look at the actual difference after taxes and deductions. A $5,000 raise does not mean $5,000 lands in checking. The usable monthly increase may be smaller than the headline number.

Once you know the real increase, you can make a plan.

This pause matters because lifestyle creep moves fast. If every extra dollar gets absorbed before you name it, the raise may not improve your financial position much at all.

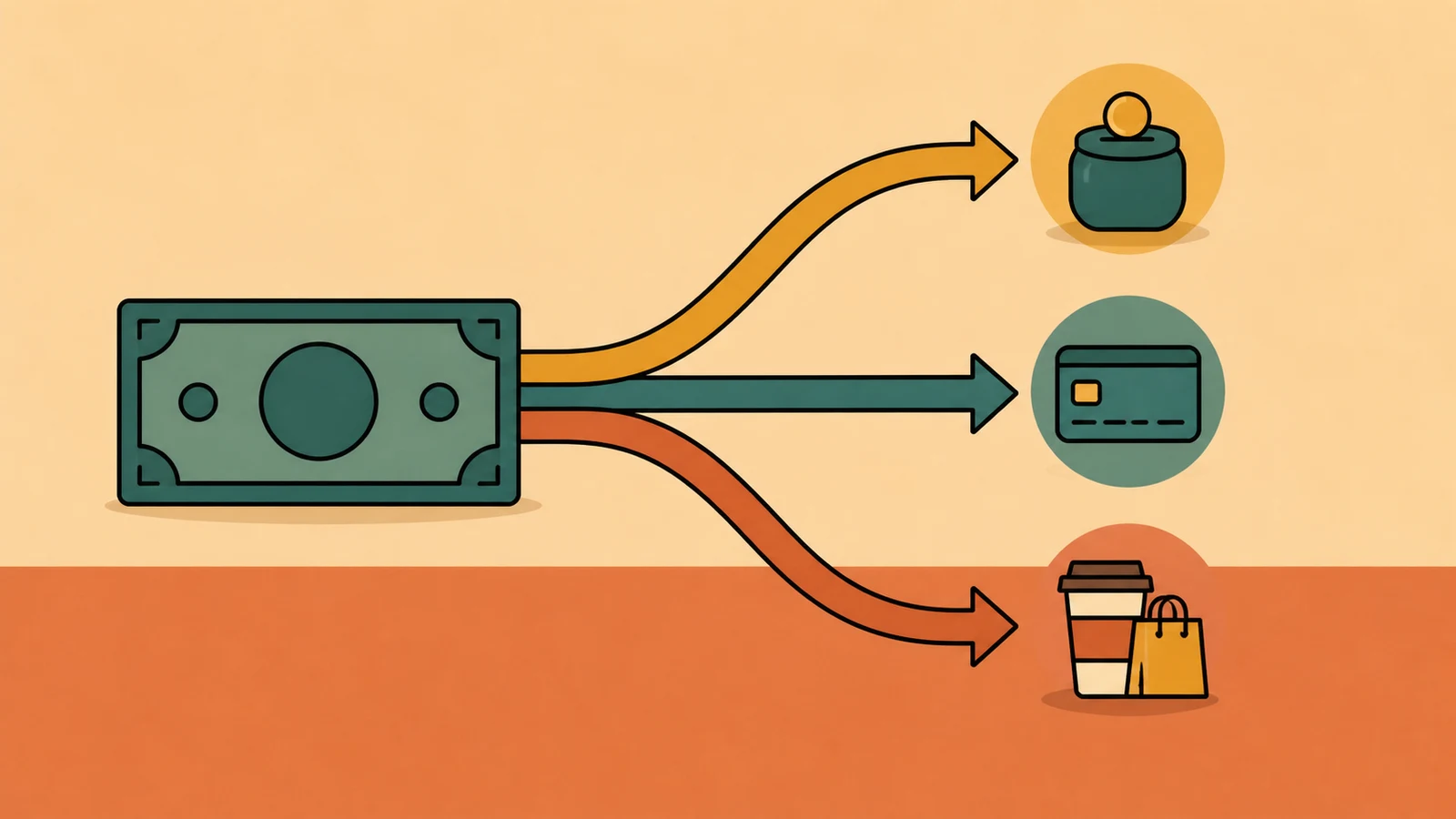

Split The Raise

You do not have to save every dollar of a raise.

You also probably do not want to spend every dollar of it.

Try splitting the increase into three jobs:

- Improve the present.

- Strengthen the foundation.

- Build the future.

Improve the present means you get to enjoy some of the raise. That is allowed. A raise is not only a homework assignment.

Strengthen the foundation might mean emergency savings, a bill buffer, or high-interest debt payoff.

Build the future might mean retirement contributions, investing, a 529 plan, or another long-term goal once the basics are stable.

Pick Percentages Before Purchases

Percentages can keep the decision simple.

For example:

- 50% to savings or debt payoff.

- 30% to better everyday life.

- 20% to long-term investing or another goal.

That is only an example. The right split depends on your situation. If you have no emergency savings, more may need to go toward a cushion. If high-interest credit card debt is growing, debt may deserve the first strong move. If your foundation is solid, investing may get a larger share.

The useful part is choosing the split before the raise becomes invisible.

Upgrade On Purpose

Lifestyle creep is not the same as enjoying your life.

An intentional upgrade can be great. Maybe the raise pays for a gym you will actually use, better childcare coverage, a safer car repair plan, or one dinner out each week without guilt.

The problem is unconscious upgrading. That is when every category quietly expands and none of the extra income builds anything.

Choose the upgrades that matter. Let the rest wait.

Automate The Serious Part

Once you choose the savings, debt, or investing amount, automate it if possible.

Set the transfer near payday. Increase the debt payment. Raise the retirement contribution. Move the increase before the new normal gets comfortable.

This is the same reason automatic saving works for smaller goals. The system makes the decision before the day gets busy.

You can still adjust later. Automation is a steering wheel, not a locked door.

Watch The First Three Months

The first three months after a raise are useful.

Check whether the extra income is doing what you wanted. Did savings grow? Did debt fall? Did spending rise in categories you actually care about? Did the raise reduce stress, or did the baseline just get more expensive?

No shame. Just information.

If the raise disappeared, reset the split. If the plan worked, keep it moving.

Try This

When your next raise, bonus, or income bump arrives, write down the after-tax monthly increase.

Then assign it before spending it:

$___ for today, $___ for stability, $___ for the future.

Enjoy part of the raise on purpose. Let the rest make your life sturdier.