A Budget For People Who Hate Budgeting

A simple way to plan income, bills, and spending when detailed categories make you want to quit.

Some people hear the word budget and immediately picture a spreadsheet with 47 categories and the emotional warmth of a parking ticket.

Fair.

Budgeting can get overbuilt fast. But the useful version is much simpler: a budget is just a plan for each paycheck before it wanders off.

If detailed tracking makes you quit, try a smaller version.

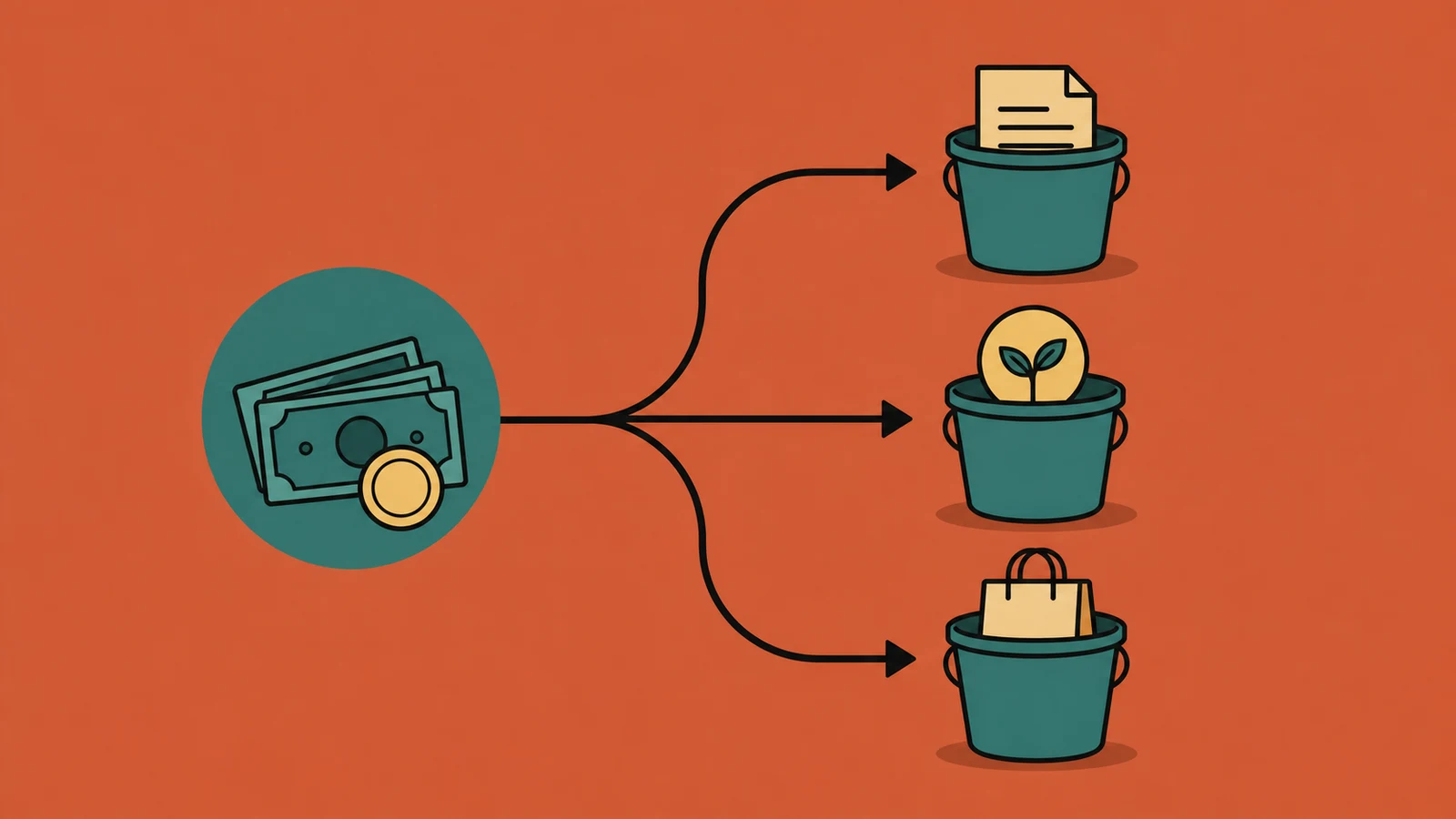

Start With Three Numbers

You do not need to name every dollar on day one.

Start with three numbers:

- Required bills.

- Savings or debt payoff.

- Flexible spending.

Required bills are the payments that keep life running: rent or mortgage, utilities, insurance, transportation, minimum debt payments, childcare, groceries, and anything else that has to be handled.

Savings or debt payoff is the amount you want to move on purpose. That might be a starter emergency fund, an extra credit card payment, or a small automatic transfer toward your first savings cushion.

Flexible spending is the amount left for everything else.

That last number is the one people usually need most. It tells you what life can cost after the required stuff is handled.

Build Around The Next Paycheck

A monthly budget can be useful, but when you are starting out, a paycheck plan often matters first.

Ask:

- What income is coming in next?

- What has to be paid before the following paycheck?

- What do I want to save or pay down?

- What is left for flexible spending?

This keeps the plan close to reality. If rent is due before the next paycheck, rent comes first. If groceries need to last eight days, the grocery number needs to reflect eight days. A budget that ignores timing can look fine on paper and still fail in real life.

Every paycheck has dates attached. The plan should, too.

Use Fewer Categories

If categories help you, use them. If they make you want to disappear into a couch cushion, use fewer.

You might only need:

- Bills

- Food

- Transportation

- Savings

- Debt

- Everything else

That is enough to begin. You can add detail later if it would help you make better decisions.

The point of tracking is not to create a museum of receipts. The point is to notice patterns. If “everything else” keeps breaking the plan, then you can split it into restaurants, shopping, subscriptions, or whatever category is causing the leak.

Let the problem earn the extra detail.

Give Yourself A Realistic Flex Number

A budget that includes no flexible spending is usually just a delay button.

People need some room for normal life. Coffee, school events, birthday gifts, a quick lunch, a small treat after a hard week. If the plan pretends those things will never happen, they will still happen, but now they will feel like failure.

Put a realistic flexible spending number in the plan.

If the number is small, that is okay. Clear is better than imaginary. You can decide how to use it instead of being surprised when it disappears.

Check Once A Week

Daily tracking works for some people. Other people would rather alphabetize soup cans.

A weekly check-in is often enough.

Pick one day and look at:

- What bills cleared.

- What spending surprised you.

- How much flexible spending is left.

- Whether the next transfer still works.

This should take 10 to 15 minutes. The goal is to steer while there is still time to adjust, not to review the month after the paycheck is gone.

Try This This Week

Before your next paycheck, write down the three numbers: required bills, savings or debt payoff, and flexible spending.

Do not make it perfect. Make it honest.

If you can see those three numbers, you have the beginning of a budget. Not a dramatic one. A useful one, which is better.